Intel's Hala Point neuromorphic computing system deployed 1.15 billion artificial neurons in production environments, marking the transition from research prototypes to commercial brain-inspired computing infrastructure. The deployment coincides with BrainChip's Akida chips entering production applications across IoT and edge computing markets.

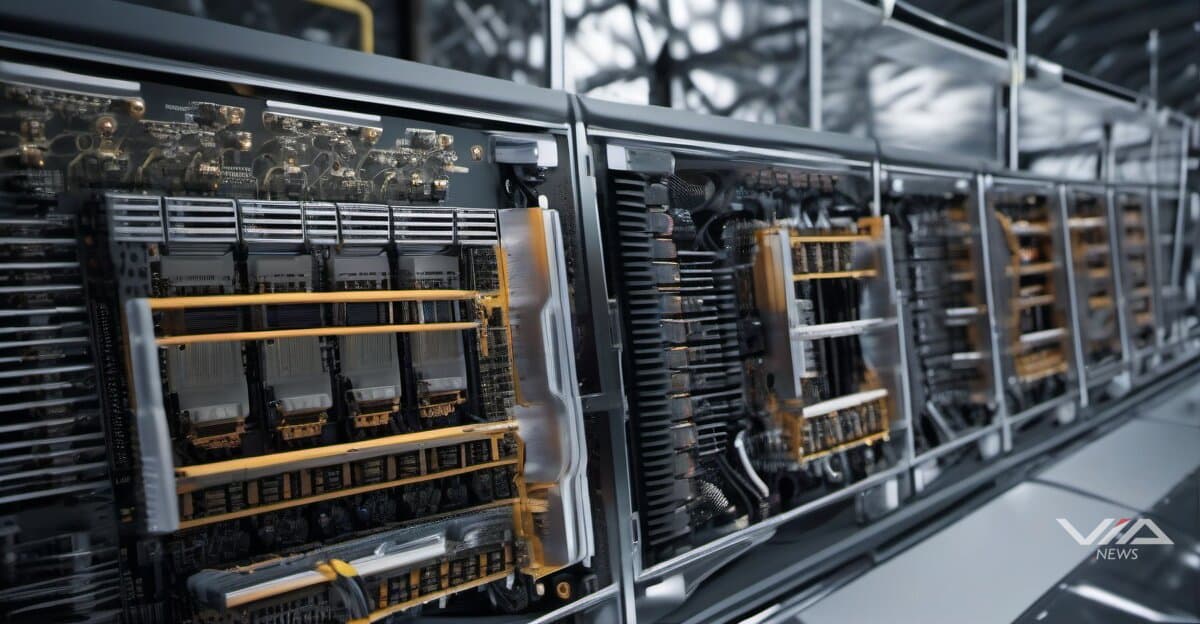

Amkor Technology committed $2 billion to build an advanced packaging campus in Arizona, scheduled to begin operations in 2028. The facility addresses growing demand for specialized chip packaging required by AI accelerators and high-performance computing systems. Advanced packaging enables multiple chiplets to communicate at speeds approaching monolithic designs while improving yields and reducing costs.

NVIDIA extended its GPU roadmap through 2027 with the Rubin Ultra architecture, maintaining its accelerator development cadence. Corvex integrated confidential computing capabilities into NVIDIA's HGX B200 platform, adding hardware-level security for sensitive enterprise AI workloads. The combination addresses financial services and healthcare requirements for processing encrypted data without exposing information to system operators.

VCI Global launched its Intelli-X enterprise AI platform, designed for production deployment across data center environments. The platform integrates with existing infrastructure management tools and supports multiple accelerator architectures. Enterprise adoption signals movement beyond pilot projects to scaled implementations with service-level requirements.

Aehr Test Systems reported $6.5 million in bookings during the first six weeks of Q3 fiscal 2026, with orders for high-power Sonoma test configurations handling up to 2,000 watts per device. The company forecasts $60-80 million in bookings for the second half of fiscal 2026, primarily from AI wafer-level and packaged-part burn-in testing. A lead production customer provided forecasts for AI ASIC shipments beginning Q1 fiscal 2027.

The infrastructure buildout spans manufacturing capacity, specialized architectures, and enterprise software layers. Combined investments indicate market participants preparing for sustained AI hardware demand rather than experimental deployments. Packaging capacity additions address physical integration challenges while neuromorphic approaches target power efficiency constraints in edge applications where traditional architectures face limitations.